The Owned Pipeline: What Mortgage Marketing Looks Like in the Post-Trigger Era

For ten years, the mortgage industry rented its leads.

Trigger leads, internet leads, aged lists, intent-based platforms. The model was simple. Pay someone who owned the borrower relationship before you did, and pay again for the next one when the first one did not fund.

That model is over.

The Homebuyers Privacy Protection Act took the largest single source of rented leads off the table in March. Internet lead prices have risen 45 percent year over year on some platforms, with continued increases as the displaced trigger lead budget reallocates into a finite supply pool. Vendor calls have intensified. Every week brings a new pitch for the next compliant alternative.

The mistake most lenders are making right now is treating this as a sourcing problem. It is not. It is a model problem. The lenders who will be cost-competitive in 2027 and 2028 are the ones who, starting in 2026, build a pipeline they own instead of one they rent.

WHAT “OWNED” ACTUALLY MEANS

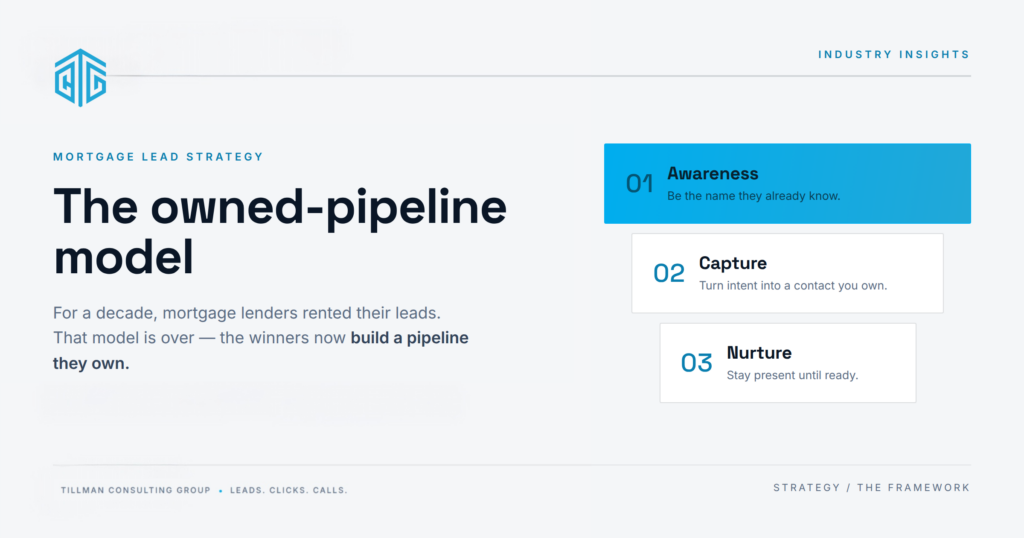

An owned pipeline has three layers. None of them are new. What is new is that the industry no longer has the option of skipping any of them.

LAYER ONE: AWARENESS

The borrower needs to know who you are before they need you. Most mortgage lenders skip this entirely. The thinking has been that consumers shop on rate, so brand does not matter. That thinking was always wrong, and it is now expensive.

A borrower deciding between two lenders with similar rate offers will choose the one they have heard of. The lender they have heard of is the one who has been showing up on social, in their inbox, in the local market, with point of view, for months before the moment of intent.

Brand awareness for mortgage is not running a billboard. It is sustained presence in the channels where your borrowers live, with content that earns the next click instead of buying it.

LAYER TWO: CAPTURE

When intent converts to action, the borrower has to land somewhere that does not lose them. This is the part most lenders think they have solved and most have not.

Pages that load fast instead of slow. Forms that ask less to get more. Routing that gets the right person on the phone inside the contact window that matters. Campaigns that target the specific moments of borrower intent that are actually worth bidding on, not the broad demographic categories that everyone is already paying for.

The capture layer is where acquisition spend actually pays for itself. Done well, it cuts cost per qualified lead. Done poorly, it is where most of the budget leaks out.

LAYER THREE: NURTURE

The borrower rarely funds on the first interaction. Industry data has shown this for two decades. A meaningful portion of leads that enter the funnel will fund eventually, on a timeline that does not match the lender’s quarterly reporting cycle.

The nurture layer is the system that stays in touch with those borrowers, with relevance, across weeks and months. Sequences that match where the borrower is in their decision process. Channels they actually open. Outreach that respects compliance and respects the borrower’s time. Retargeting that brings the warm lead back when their situation changes.

This is the layer that turns the same acquisition spend into two or three times the funded volume, by extracting value from leads that the bought-list model treated as one-and-done.

WHY THIS IS BUILT, NOT BOUGHT

There is no vendor that sells “an owned pipeline.” It is built. That is what makes it a moat.

Every layer requires decisions, investment, and operational discipline that compounds over time. The brand presence built over six months gets stronger in month seven. The nurture sequence iterated over a year converts better than the one launched yesterday. The capture infrastructure tuned to the lender’s specific borrower mix outperforms the generic stack.

The lenders who start building this now will spend 2028 with a unit economics profile their competitors cannot match by writing a bigger check.

WHAT THIS LOOKS LIKE IN PRACTICE

At Tillman Consulting Group, this is the conversation we are having with every client in 2026.

The work we bring to every engagement is more than twenty-five years of pattern recognition across all three layers. We have seen them built well. We have seen them built poorly. We have seen what compounds and what stalls. That experience is the strategic frame I bring directly to each client.

The execution that builds each layer requires specialists. I have worked alongside the right operators for years. With strategic clarity and successful execution, The client ends up with a pipeline they own, built by people who know how to build each piece.

WHERE TO START

If the model above is the destination, the question is where a lender starts. Three places, in order of urgency for most mid-size operations.

1. AUDIT THE THREE LAYERS HONESTLY. Where is the team strongest? Where is the team weakest? Most lenders are strongest at capture, middling at nurture, and almost absent at awareness. The weakest layer is usually the one to invest in first, because the system is only as strong as its weakest link.

2. STOP PRETENDING THE BOUGHT-LEAD MODEL CAN BE RESURRECTED. Every dollar spent chasing the next “trigger lead alternative” is a dollar not spent building the owned pipeline. Some lenders will keep buying. They will lose, slowly, and then all at once.

3. PICK A SIX-MONTH HORIZON, NOT A QUARTER. Owned pipelines do not generate ROI in 60 days. They generate compounding ROI starting around month four and accelerating from there. The lenders who commit to that horizon now will be the ones with a defensible business in 2028.

THE ERA WE ARE IN

The trigger lead era rewarded speed and volume. The era that started March 5 rewards depth and ownership. The first move in that game is recognizing it is a different game, and resourcing for it accordingly.

If you are working through what the owned-pipeline model looks like for your specific operation, that is the conversation Tillman Consulting Group is built for.